DSCR formula, DSCR full form, Ideal DSCR for Banks. If you are applying for a term loan, then you should know all bout DSCR. This article covers everything you need to know about DSCR and also how you can get the ideal DSCR ratio for a bank loan.

Tutorial Video

DSCR meaning

DSCR full form is Debt Service Coverage Ratio. In simple terms, DSCR means a ratio that shows how well you can repay (service) the loan (principal + interest) in the given year. After taking a term loan from a bank, you have to repay it by EMI payments. DSCR ratio checks whether you have earned sufficient profits to make these EMI payments comfortably.

So higher the DSCR, the more financially sound your business is to repay the loan.

DSCR formula. How to calculate DSCR

The most common DSCR formula used in India is:

Auto calculate DSCR with Fortrisk Project Report Software

If you are using our Project Report software, do not worry; our software will automatically calculate the DSCR ratio for you as per Bank format.

Click here to Make a Project Report for Bank Loan with automatic DSCR calculation.

Ideal DSCR ratio for Banks in India

In most cases, banks consider DSCR in the range of 1.3 to 5 as the ideal ratio range.

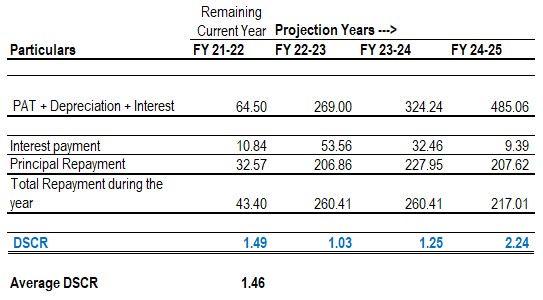

Also, the banks pay more importance to the average DSCR of the entire loan period than the year-on-year DSCR. Below example shows how to calculate the average DSCR:

As seen in the above table, the average DSCR is 1.22, and it is very different from the DSCR ratio of each year. In the initial years, you may incur losses, and the DSCR value may be lower than 1.0. But in future years, profitability will be good to repay the loan. As a result, for banks, the average DSCR is more important.

Steps to get a good DSCR ratio

If you are not getting the dscr ratio in the ideal range of 1.5 to 5, then you can improve your dscr with these simple steps

DSCR is too low.

If you are getting a DSCR of less than 1, you are not earning enough to repay the loan, and hence the bank will not be able to sanction your loan as it becomes risky.

Don’t worry; with our project report software, you can quickly improve the DSCR value in your report in a few easy steps.

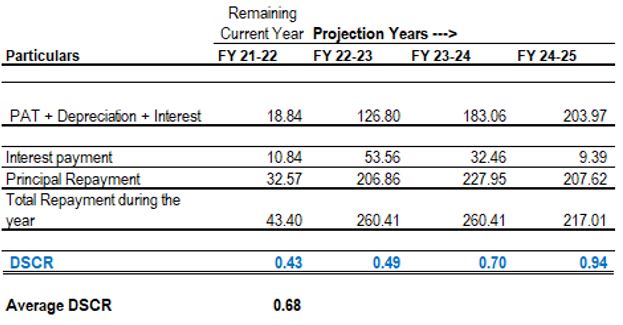

Let’s take the below case as an example in which our DSCR is presently coming at 0.68

Now, let’s see how we can improve this DSCR value with Fortrisk Project Report Software.

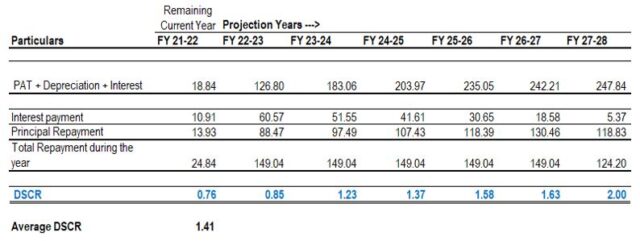

1. Increase the Loan Duration

It can be a case that your business will take time to earn a steady income. It is always better to apply for a loan with a longer repayment duration in such a case.

By changing the loan repayment period from 3 to 7 years in our example case, you can see the DSCR has drastically improved to 1.41.

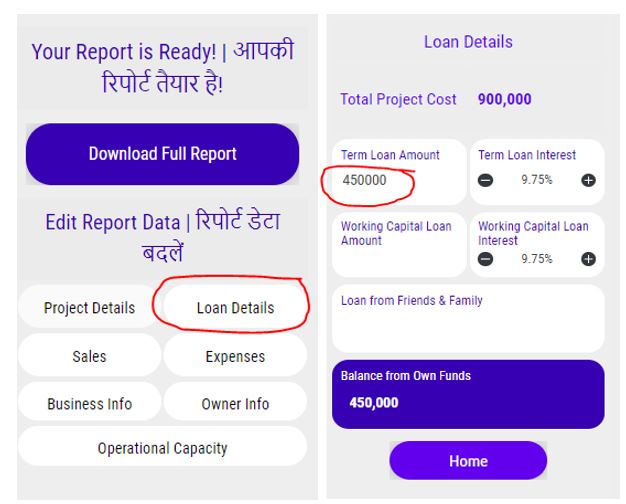

2. Change the loan and own capital proportion

Another easy technique to improve your DSCR is to reduce the proportion of loan amount and increase your capital contribution in the project.

Continuing with the same example, we got a DSCR value of 0.68 with the loan and own funds contribution as below.

In our software, click the “Loan Details” button. Enter a revised loan amount. In this example, let’s change the term loan value from Rs. 6,75,000/- to Rs. 4,50,000/-

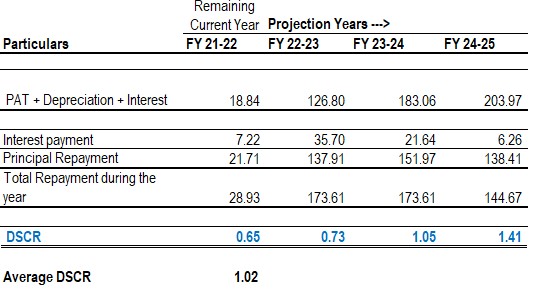

With just this change, the new DSCR has now increased from 0.68 to 1.02

3. Revise Sales Projections

Our software automatically calculates sales projections for you. If your DSCR value is low, look at the sales values. In our example, the software computed sales are:

If you expect to earn more sales, you can change the sales projections in our software by clicking the sales button and changing the sales value.

With this change, our DSCR value has now significantly improved from 0.68 to 1.46

So, with Fortrisk Project Report software, you can now improve your Project Report’s DSCR value with these easy techniques in no time and effort.

What if the DSCR value is too high?

Earlier, we have said that higher the DSCR means better your business’s capacity to pay off the loan. So you will say that the higher, the better for DSCR, but that is not the case. A very high DSCR value would mean that you earn enough and don’t need a loan.

Generally, the average DSCR value of more than 5.0 is considered high by Banks, and they may hesitate to sanction your loan.

Don’t worry. You can correct a high DSCR value using the same steps discussed above. In other words, in Fortrisk Project Report software, you can

Reduce the Loan Duration period

Increase the Loan proportion vis-à-vis own capital

Scale down the sales projections

We hope this article helped you learn all about DSCR and how easily you can improve the DSCR value in your loan’s project report. If you liked this article, please also subscribe to our YouTube Channel.

If you want our experts to prepare your Project Report and CMA Data, then do check out our premium plans.

4 comments

Tilok

April 21, 2022 at 10:38 am

How to download Project Report after payment

mithishah

April 22, 2022 at 5:51 am

Sir after making the payment, kindly log in and click the Pro plan button. Enter your business details online and then you will get option to download your report. Click the download button to get your full project report

Hitesh jain

September 26, 2022 at 10:11 am

Hi,

I am developing a residential layout for which I am looking for financing from banks .

Would require a project report with admissible DSCR .

mithishah

September 30, 2022 at 6:59 am

sir, you can make a project report yourself by using our online software. For that please see the demo video in the below link 👇🏽.

https://youtu.be/3DnuxcUof5k

Another option is our premium plan in which our CA expert team will make a more detailed and customized report for you (please see our pricing page for more details)

https://fortriskconsulting.com/pricing/